Welcome to our guide on exploring business loan options! If you’re a small business owner or entrepreneur looking to take your business to the next level, you may be considering taking out a loan to fund your growth. With so many different options available, it can be overwhelming to know where to start. In this article, we will walk you through the process of making inquiries about business loans, so you can make an informed decision that aligns with your business goals.

Understanding Business Loans

When starting or expanding a business, one of the most crucial aspects to consider is securing funding. Business loans are a common way for entrepreneurs to finance their ventures, whether it be for purchasing equipment, hiring employees, expanding operations, or covering operating expenses. Understanding the ins and outs of business loans can help you make informed decisions that will benefit your company in the long run.

Business loans come in various forms, each tailored to meet different business needs. Some common types of business loans include term loans, lines of credit, SBA loans, equipment financing, and merchant cash advances. Term loans are a lump sum of money that is repaid over a set period of time with a fixed interest rate. Lines of credit, on the other hand, provide businesses with access to funds that can be used as needed, similar to a credit card. SBA loans are government-backed loans that offer favorable terms to small businesses. Equipment financing allows you to purchase or lease equipment for your business, while merchant cash advances provide a lump sum of cash upfront in exchange for a percentage of future credit card sales.

Before applying for a business loan, it is important to assess your business’s financial needs and determine how much funding you require. You should also consider your ability to repay the loan, including factors such as your cash flow, revenue projections, and credit history. Lenders will evaluate your business’s creditworthiness before approving your loan application, so it is crucial to have your financial documents in order, such as balance sheets, profit and loss statements, tax returns, and business plans.

When researching potential lenders, consider factors such as interest rates, fees, repayment terms, and customer reviews. It is advisable to compare multiple loan offers and negotiate with lenders to secure the best terms for your business. Additionally, be cautious of predatory lenders who may offer high-interest loans with unfavorable terms that could put your business at risk.

Once you have secured a business loan, it is important to use the funds wisely to achieve your business goals. Whether you are using the loan to launch a new product, hire employees, or expand your operations, make sure to track your expenses and monitor your progress towards your objectives. By effectively managing your business loan, you can position your company for success and growth in the competitive marketplace.

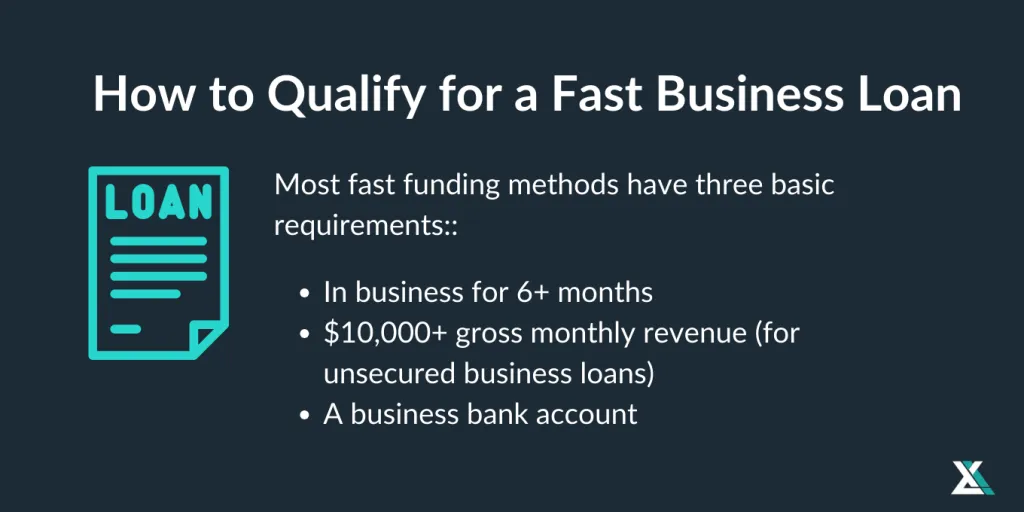

How to Qualify for a Business Loan

Qualifying for a business loan can seem like a daunting task, but with the right preparation and understanding of the process, you can increase your chances of securing the funding you need. Here are some key factors to consider when applying for a business loan:

Credit Score: One of the most important factors that lenders consider when reviewing a business loan application is the borrower’s credit score. A good credit score demonstrates to lenders that you are a responsible borrower and are likely to repay the loan on time. Make sure to check your credit report and score before applying for a business loan and take steps to improve it if necessary. This may include paying off any outstanding debts, reducing credit card balances, and making payments on time.

Business Plan: Lenders want to see a solid business plan that outlines your goals, strategies, and financial projections. Your business plan should demonstrate a clear understanding of your industry, target market, and competition. It should also include a detailed financial forecast that shows how you plan to use the loan funds and how you expect to generate revenue to repay the loan. A well-thought-out business plan can help lenders feel confident in your ability to manage and grow your business successfully.

Cash Flow: Lenders will also assess your business’s cash flow to determine your ability to repay the loan. Your cash flow statement should show a positive trend, with enough income to cover your operating expenses, debt payments, and loan repayments. If your cash flow is inconsistent or negative, lenders may be hesitant to approve your loan application. Take steps to improve your cash flow before applying for a business loan, such as cutting costs, increasing revenue, or securing additional sources of funding.

Collateral: Some lenders may require collateral to secure a business loan, especially if you have a limited credit history or are seeking a large loan amount. Collateral can include assets such as real estate, equipment, inventory, or accounts receivable that can be used to secure the loan in case of default. Be prepared to provide details about the value of the collateral and how it will be used to secure the loan. Keep in mind that if you default on the loan, the lender has the right to seize the collateral to recoup their losses.

Industry Experience: Lenders may also look at your industry experience when evaluating your loan application. Having a strong track record in your industry can give lenders confidence that you have the knowledge and skills to successfully manage and grow your business. If you are a new entrepreneur or entering a new industry, consider partnering with a mentor or advisor who can provide guidance and support as you navigate the challenges of running a business. Demonstrating a commitment to learning and growing in your industry can help strengthen your loan application.

Comparing Different Types of Business Loans

When it comes to obtaining a business loan, it is important for entrepreneurs to be aware of the different types of loans available to them. Each type of loan caters to specific needs and requirements, so it is essential to understand the differences between them in order to make an informed decision. Here, we will explore and compare the various types of business loans:

1. Traditional Bank Loans: Traditional bank loans are the most common type of business loan. They typically require a good credit score and a solid business plan in order to qualify. The interest rates for traditional bank loans tend to be lower compared to other types of loans, making them an attractive option for well-established businesses with a strong financial history.

2. SBA Loans: Small Business Administration (SBA) loans are government-backed loans designed to help small businesses access funding. These loans often have more flexible terms and lower down payment requirements compared to traditional bank loans. However, the application process for SBA loans can be more rigorous and time-consuming.

3. Online Alternative Lenders: Online alternative lenders have become increasingly popular in recent years due to their quick and easy application process. These lenders typically offer short-term loans with higher interest rates compared to traditional bank loans. While online alternative lenders may be a good option for businesses with less-than-perfect credit or those in need of fast funding, it is important to carefully review the terms and conditions before agreeing to the loan.

4. Equipment Financing: Equipment financing is a type of loan specifically used for purchasing new equipment or machinery for the business. The equipment itself serves as collateral for the loan, making it a lower-risk option for lenders. Businesses that rely heavily on equipment, such as construction companies or manufacturers, may benefit from equipment financing.

5. Invoice Financing: Invoice financing, also known as accounts receivable financing, allows businesses to receive a cash advance based on their outstanding invoices. This type of loan can help businesses improve cash flow and cover operating expenses while waiting for customers to pay their invoices. Invoice financing is a popular option for businesses with long payment cycles or seasonal fluctuations in revenue.

Overall, understanding the differences between the various types of business loans is crucial for entrepreneurs looking to secure funding for their ventures. By carefully evaluating the specific needs of their business and comparing the terms and rates of different loan options, entrepreneurs can make an informed decision that best suits their financial goals.

Important Factors to Consider Before Applying for a Business Loan

When considering applying for a business loan, there are several important factors that you should take into account to ensure that you make the best decision for your company. Here are some key things to consider before you start the application process:

1. Reason for the Loan: Before applying for a business loan, it is essential to have a clear understanding of why you need the funds and how they will be used. Whether it is to expand operations, purchase new equipment, cover unexpected expenses, or any other reason, knowing the purpose of the loan will help you determine the amount you need and the type of loan that is best suited for your needs.

2. Financial Health of Your Business: Lenders will want to assess the financial health of your business before approving a loan. Make sure to have current financial statements, profit and loss statements, and cash flow projections ready to demonstrate your company’s ability to repay the loan. A strong financial track record will increase your chances of securing a loan with favorable terms.

3. Credit Score: Your personal and business credit scores play a significant role in the loan application process. Lenders use these scores to evaluate your creditworthiness and determine the interest rate and terms of the loan. Make sure to check your credit scores and address any issues or discrepancies before applying for a loan. A higher credit score will increase your chances of getting approved for a loan with better terms.

4. Collateral: In some cases, lenders may require collateral to secure a business loan. Collateral can be in the form of business assets, equipment, real estate, or other valuable items that the lender can claim in case of default. Before applying for a loan, consider what assets you are willing to use as collateral and make sure that you have a clear understanding of the potential risks involved. It is important to assess the value of your collateral and ensure that it is sufficient to cover the loan amount.

By carefully considering these important factors before applying for a business loan, you can increase your chances of securing the funding you need on favorable terms. It is essential to do thorough research, compare different loan options, and consult with financial advisors to make an informed decision that will benefit your business in the long run.

Tips for a Successful Business Loan Application

Applying for a business loan can be a daunting process, but with the right preparation and strategy, you can increase your chances of success. Here are some tips to help you navigate the application process and secure the funding you need for your business:

1. Understand your business needs: Before you apply for a loan, take the time to assess your business needs. Consider why you need the funding, how much you need, and how you plan to use the money. This will help you choose the right type of loan and present a clear case to potential lenders.

2. Check your credit score: Your credit score is one of the key factors that lenders consider when evaluating your loan application. Before you apply for a business loan, check your credit score and take steps to improve it if necessary. A higher credit score can increase your chances of approval and help you secure better loan terms.

3. Gather all necessary documents: Lenders will require a variety of documents to evaluate your loan application, including financial statements, tax returns, business plans, and more. Gather all necessary documents before you apply to expedite the process and demonstrate your financial stability and business acumen.

4. Shop around for the best loan options: There are many lenders and loan products available in the market, so it’s important to shop around and compare your options before making a decision. Consider factors such as interest rates, fees, repayment terms, and eligibility requirements to find the best loan for your business.

5. Build a strong relationship with your lender: Building a strong relationship with your lender can help you throughout the loan application process and beyond. Take the time to meet with potential lenders, ask questions, and communicate your business goals and challenges openly. This can help you establish trust and show that you are a reliable borrower.

By following these tips and being proactive in your loan application process, you can increase your chances of success and secure the funding you need to grow your business. Remember to stay organized, prepared, and open to feedback from lenders to make the application process as smooth as possible.

Originally posted 2025-08-01 21:28:02.